Being in a car accident can be a jarring and overwhelming experience. Navigating Nevada’s at-fault insurance rules requires a clear understanding of your rights, which isn’t always easy in the aftermath of a crash. Knowing how insurance claims typically work in Nevada can make the process more manageable.

Here in Las Vegas, we see firsthand the legal and logistical challenges that follow the city’s 20,000+ auto accidents each year. Many victims face pushback from insurers and delays in compensation. When an insurer refuses to accept liability, it helps to understand how to respond when a claim is denied by the at-fault driver’s insurance.

| Key Takeaways | |

|---|---|

| Nevada Insurance System | – Nevada uses an at-fault insurance system – The at-fault driver is liable for damages caused |

| Determining Fault | – Police investigations – Accident reconstruction – Witness statements – Comparative negligence rules |

| Filing a Claim | – Report incident promptly – Gather evidence like medical records – Submit demand letter with documentation – Get an attorney to maximize payout |

| Insurance Requirements | – $25K/$50K bodily injury liability – $20K property damage liability – $25K/$50K uninsured motorist coverage |

| After an Accident | – Exchange information with other drivers – Call police, report incident – Document injuries, losses – Consult attorney before recorded statement |

| Hiring a Lawyer | – Levels the playing field against insurers – Fights for maximum compensation – Takes case to court if necessary |

| Damages | – Medical expenses – Property losses – Lost income – Pain and suffering |

| Statute of Limitations | – 2 years from date of injury to file claim |

Having an experienced personal injury attorney can make all the difference in these situations. Someone like Jack Bernstein, who has successfully represented accident victims for over 40 years. He understands the nuances of prevailing within Nevada’s at-fault insurance system in order to get clients the maximum compensation they deserve.

No-Fault vs At-Fault States: Understanding the Difference

When it comes to auto insurance, states fall into one of two systems: no-fault or at-fault.

- No-Fault States: In a no-fault insurance system, each driver’s own insurance company pays for their injuries and vehicle damage regardless of who was at fault for the accident. For example, if you’re hit by a reckless driver in a no-fault state, you deal directly with your insurer to get compensated.

- At-Fault States: In an at-fault insurance system, the at-fault driver’s insurer pays for the damages they caused. For instance, if someone runs a red light and hits your car, their insurance covers your losses.

- Impact on Premiums: No-fault states generally have lower insurance premiums, though coverage amounts may be restricted. At-fault states can have higher premiums due to increased litigation risks.

- Policyholder Rights: No-fault systems limit your ability to sue a negligent driver. At-fault systems give more legal options if you are not at fault.

Both models have trade-offs. No-fault systems typically resolve claims faster but limit total compensation. At-fault systems allow more complete recovery but may involve longer legal processes. To see where Nevada stands, it helps to know how its insurance framework is structured.

Nevada’s At-Fault Laws

Nevada operates under an at-fault auto insurance system. This means the at-fault driver and their insurer are responsible for covering the losses they cause in an accident.

- For the not-at-fault driver, this allows you to recover both economic and non-economic damages through a liability claim or lawsuit.

- Economic damages include medical bills, lost wages, vehicle repair costs, etc.

- Non-economic damages cover pain and suffering, mental anguish, and diminished quality of life.

- Nevada is also a “pure comparative negligence state.” This means you can recover damages even if you were partially at fault, reduced by your percentage of fault.

At-fault laws affect both claimants and defendants:

- For claimants, the at-fault driver’s insurer is responsible for covering damages. But when offers fall short of what’s fair, working with an attorney can help improve the outcome—especially when it comes to disputing an insurance company’s determination of fault.

- For defendants, you are accountable for all damages caused by your negligence. Your insurer will defend against exaggerated or fraudulent claims, but valid claims must be paid. Having strong liability coverage is essential.

Common scenarios under Nevada’s at-fault system include:

- Multi-vehicle accidents with complex fault disputes

- Accidents with uninsured/underinsured motorists

- Hit-and-run collisions where the at-fault driver flees

- Catastrophic injuries requiring extensive care

Determining Fault in Nevada Auto Accidents

Who’s at fault in an accident is not always clear cut. Fault determination often involves:

- Police Investigations – Officers will assess the accident scene, take statements from parties involved, and issue citations if warranted. However, police reports contain opinions on fault that may be challenged.

- Accident Reconstruction – Expert analysis of skid marks, vehicle damage, collision dynamics, etc. can help prove or disprove driver negligence. This is useful when police reports are inconclusive.

- Witness Statements – Independent eyewitnesses can provide objective accounts of fault, though memories fade over time. Recording witness names/numbers at the scene is crucial.

- Comparative Negligence – Even if you hold some fault, you can still recover damages proportional to the other driver’s negligence in Nevada.

Proving fault often involves battling against insurance companies eager to limit payouts. An experienced attorney levels the playing field by compelling insurers to pay what you rightfully deserve.

Filing a Claim in Nevada

To file an insurance claim after an accident:

- Report incident to your insurer promptly, even if not at fault. There are deadlines for initial notifications.

- Gather evidence like medical records, photo/video documentation, accident reports, etc. to support your claimed losses.

- Submit a demand letter to the at-fault driver’s insurer detailing your damages with evidence.

- Be aware insurers may dispute or delay claims. Legal help can expedite resolution and maximize your payout.

Other claim considerations:

- Deadlines – Injury claims have a two year statute of limitations in Nevada. Act quickly to preserve your rights.

- Disputes – Refusal to pay, unfair settlement offers, etc. may require litigation. Don’t accept lowballs out of desperation. Consult an attorney.

- Uninsured Motorists – Make a claim through your own UM/UIM policy if the at-fault driver has no/inadequate coverage.

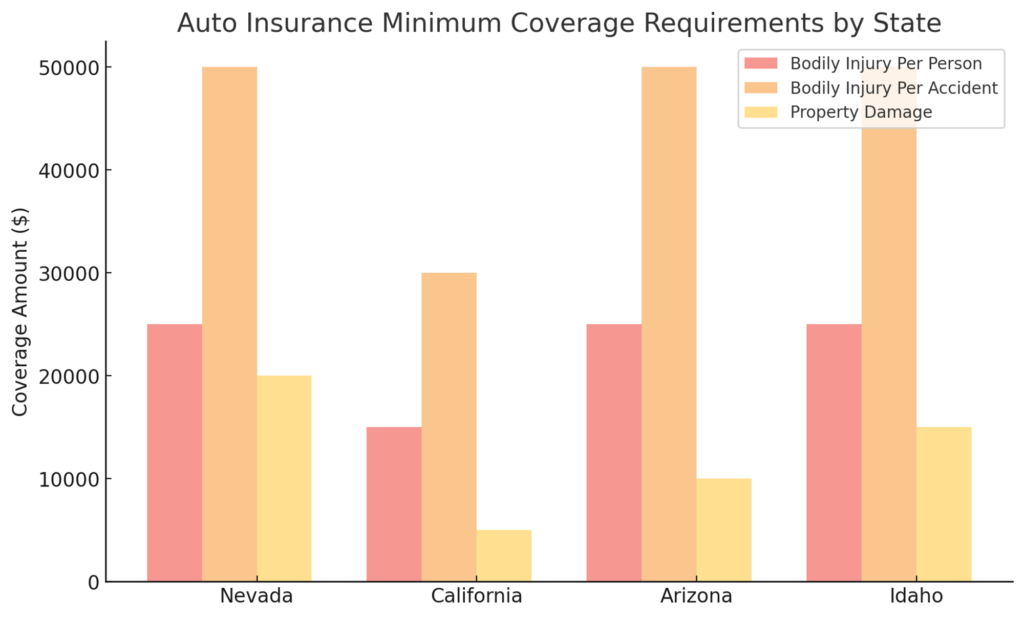

Insurance Requirements in Nevada

Nevada requires:

- Bodily Injury Liability – $25,000 per person, $50,000 per accident minimum. This covers injuries to others you cause.

- Property Damage Liability – $20,000 minimum. Covers damage to others’ property that you cause.

- Uninsured/Underinsured Motorist (UM/UIM) – $25,000 per person, $50,000 per accident minimum. Protects you if hit by an uninsured or underinsured driver. Crucial coverage in Nevada given high rates of uninsured drivers.

How Nevada compares:

- California has lower minimum bodily injury liability limits ($15,000/$30,000). Property damage minimum is also lower at $5,000.

- Arizona matches Nevada’s bodily injury minimums ($25,000/$50,000) but requires just $10,000 in property damage liability.

- Idaho is similar with $25,000/$50,000 bodily injury and $15,000 property damage minimums.

Takeaway: Nevada’s auto insurance minimums are relatively low compared to potential accident costs. Purchasing higher optional limits reduces your personal financial exposure in at-fault accidents. Umbrella policies provide additional protection.

Choosing the Right Insurance

Consider your unique situation and risks to determine adequate coverage:

- Age, driving history, vehicle type – major rating factors that impact premium costs. High-risk drivers pay more.

- Policy limits – higher liability coverage reduces personal assets at risk if you cause an accident. But premiums increase too.

- Deductibles – choosing a higher deductible lowers your premiums but means you pay more out-of-pocket on claims before coverage kicks in.

- Uninsured motorist protection – critically important given Nevada’s high rate of around 16% uninsured drivers. Don’t skimp here.

Consult an independent insurance agent or attorney to review your risks and guide you in choosing customized, cost-effective coverage.

After an Accident in Nevada

- Exchange driver’s license, registration, and insurance information with the other driver(s) involved. Obtain their full name, address, plate details as well.

- Call the police and report the accident promptly. Ensure you get the police report number for insurance purposes later.

- Take photos documenting property damage, skid marks, debris, injuries, etc. Photograph the scene from multiple angles before cars are moved.

- Seek medical attention for any injuries immediately, even if they seem minor at first. Delays hurt your ability to recover damages later.

- Report the incident to your insurance provider right away. There are strict notification deadlines. Preserve evidence from the scene to share.

- Keep meticulous records documenting accident-related costs like medical bills, auto repair invoices, lost wages due to missed work, etc.

- Consult an attorney before providing any recorded statement to insurance adjusters. They may try to twist your words against you.

- Watch for premium hikes at renewal after filing a claim, even if the accident was not your fault. Insurers often raise rates after any incident.

The Role of a Personal Injury Lawyer

After an auto accident, injury victims face an uphill battle getting fair compensation from insurance companies. Adjusters employ tactics to minimize payouts, including:

- Delaying claims

- Disputing liability

- Undervaluing injuries and damages

- Making lowball offers

A personal injury attorney levels this uneven playing field and fights for your best interests. An experienced lawyer will:

- Thoroughly investigate your accident to prove liability

- Gather evidence maximizing the value of your claim

- Handle negotiations with insurers to win full, fair compensation

- Take the case to court if needed to recover deserved damages

- Facilitate alternatives like mediation to reach beneficial settlements

With a knowledgeable attorney representing you, insurance companies are less likely to take advantage. Adjusters know that experienced lawyers have the skill and resolve to litigate legitimate injury claims—often prompting more reasonable settlement offers. This dynamic plays out frequently during the litigation process for motor vehicle accidents in Nevada, where strategic pressure can make a significant difference.

Don’t go it alone against big insurance. Their goal is protecting profits, not your rights. A dedicated personal injury lawyer will battle fiercely on your behalf.

Nevada’s At-Fault Auto Insurance Laws FAQs

No-fault states require each driver’s insurer to cover their injuries, regardless of fault. At-fault states make the negligent driver’s insurer liable for damages caused.

Nevada is an at-fault state. The negligent driver who caused the accident and their insurer are responsible for covering resulting damages.

Yes, Nevada follows pure comparative negligence rules. Your damages award will be reduced by your percentage of fault.

In most cases you have two years from the date of the accident to file a personal injury lawsuit under Nevada’s statute of limitations.

Photograph damage, skid marks, car positions, traffic signals, etc. Get driver/witness contact details. Save medical records, auto repair invoices, etc.

They can maximize your payout by proving liability, valuing damages, negotiating aggressively, and taking legal action if needed against insurers.

Possibly. Insurers often raise premiums after any accident claim. An attorney can help minimize increases.

More than minimums. $100,000 per person and $300,000 per accident bodily injury liability is recommended.

Make a claim through your own uninsured/underinsured motorist coverage. An attorney can help maximize your UIM benefits.

As soon as possible. An attorney will protect your rights and guide you in taking the most strategic actions throughout the claims process.

Contact Us for a Free Consultation

If you have been injured in an accident due to negligence, contact Jack Bernstein Injury Lawyers for a free, no obligation consultation with experienced Las Vegas accident lawyers. You will gain an advocate for every stage in the claims process until you have the compensation you deserve.

Jack Bernstein Injury Lawyers is available to help you handle your injury claim in the Las Vegas metropolitan area and beyond. Jack Bernstein and his team can offer you the personalized service and legal representation you deserve after an accident.

Call us at (702) 633-3333 or contact us today for a free consultation to discuss your case.